|

Form

Name |

Description |

|

This is the form for providing

information to be furnished under Sub-section (6) of Section

195 of Income Tax Act, 1961 relating to remittance of payments

to a non-resident or to a foreign company |

|

|

This is the certificate of an

accountant to be furnished under Sub-section (6) of Section

195 of Income Tax Act, 1961 relating to remittance of payments

to a non-resident or to a foreign company |

|

|

This is the application by a person

other than a banking company for a certificate under Section

195(3) of Income Tax Act, 1961 for receipt of sums other than

interest and dividends without deduction of tax |

|

|

This is the declaration

under Sub-sections (1) and (1A) of Section 197A of Income Tax

Act, 1961, to be made by an individual or a person (not being a company or a

firm) claiming certain receipts without deduction of tax |

|

|

This is the declaration

under Sub-section (1C) of Section 197A of Income Tax Act,

1961, to be made by an individual who is of the age of sixty years or more

claiming certain receipts without deduction of tax |

|

|

Form 16

(Part A) |

Certificate for tax deducted at

source from income chargeable under the head "Salaries". |

|

Form 16

(Part B) |

Certificate for tax deducted at

source from income chargeable under the head "Salaries". |

|

Certificate for tax deducted at

source in respect of income other than Salary. |

|

|

Certificate for tax deducted at

source under section 203 on sale of Immovable Properties |

|

Form 16C is the TDS certificate to be

issued by the deductor (Tenant of property) to the deductee (Landlord of

property) in respect of the tax deducted and deposited as TDS on rent under

section 194-IB of the Income-tax Act, 1961. |

|

|

Form 16D is the TDS certificate to be

issued by the deductor to the deductee in respect of the tax deducted and

deposited as TDS under section 194M of the Income-tax Act, 1961. |

|

|

Quarterly statement of deduction of

tax in respect of Salary |

|

|

Quarterly statement of deduction of

taxin respect of payments other than Salary |

|

|

The online form

available on the TIN website for furnishing information regarding TDS on

property is termed as Form 26QB |

|

|

Form 26QC is the

challan-cum-statement for reporting the transactions liable to TDS on rent

under section 194-IB of the Income-tax Act, 1961. It is an online form

available on the TIN website. |

|

|

Form 26QD is the

challan-cum-statement for reporting the transactions liable to TDS on

PAYMENTS TO RESIDENT CONTRACTORS AND PROFESSIONALS under section 194M of the Income-tax

Act, 1961. |

|

|

Form for furnishing information with

the statement of deduction / collection of tax at source filed on computer

media for a given period |

|

|

This form is the declaration

under Sub-section (1A) of Section 206C of Income Tax

Act, 1961 to be made by a buyer for obtaining goods without collection

of tax |

|

|

This is the certificate of collection

of tax at source under Sub-section (5) of Section

206C of Income Tax Act, 1961 |

|

|

Quarterly statement of Tax Collection

at Source (TCS) under Section 206C of Income Tax Act, 1961 |

|

Quarterly statement of deduction of

tax in respect of payments other than Salary made to non-residents |

As per Section 195, every person making a payment to Non-Residents (not being a Company), or to a Foreign Company shall deduct TDS if such sum is chargeable to Income Tax and the details are required to be furnished in Form 15CA.

Who is required to file Form 15CA?

As per Rule 37BB, any person responsible for paying to a Non-Resident, not being a Company, or to a Foreign Company shall furnish such information in Form 15CA.

Is it mandatory to submit Form 15CB?

No, it is not mandatory to submit Form 15CB. Form 15CB is an event-based form to be filled only when the remittance amount exceeds ₹5 lakh during a financial year and you are required to furnish a certificate from an accountant defined as per Section 288.

Can Form 15CA be withdrawn? No, there is no option to withdraw Form 15CA.

When is Form 15CA not required to be furnished? In accordance with sub-rule (3) of Rule 37BB, information in Form 15CA is not required to be furnished in case of following transactions: Remittance is made by an individual and does not require prior approval of RBI Remittance is of the nature specified under relevant purposes code as per RBI

Which part of Form 15CA do I need to fill?

The furnishing of information for payment to Non-Residents not being a Company, or to a Foreign Company in Form 15CA has been classified into 4 parts. Depending upon the case, you will need to fill the relevant part.PART A: Where the remittance or the aggregate of such remittance does not exceed ₹5 lakh during the F.Y.PART B: Where remittance or the aggregate of such remittances exceed 5 lakh rupees during the FY and an order / certificate u/s 195(2) / 195(3) /197 of the Act has been obtained from the Assessing Officer.PART C: Where the remittance or the aggregate of such remittance exceed ₹5 lakh during the FY and a certificate in Form No 15CB from an accountant has been obtained.PART D: Where the remittance is not chargeable to tax under the Income Tax Act, 1961.

What is Form 26QB ?The online form available on the TIN website for furnishing information regarding TDS on property is termed as Form 26QBThe Finance Bill 2013 has proposed that purchaser of an immovable property (other than rural agricultural land) worth ` 50 lakh or more is required to pay withholding tax at the rate of 1% from the consideration payable to a resident transferor

Sec 194 IA of the Income Tax Act, 1961 states that for all transactions with effect from June 1, 2013, Tax @ 1% should be deducted (depending upon the Date of Payment/Credit to the Seller) by the purchaser of the property at the time of making payment of sale consideration.

How will transactions of joint parties (more than one buyer/seller) be filed in Form 26QB?Online statement cum challan Form/ Form 26QB is to be filled in by each buyer for unique buyer-seller combination for respective share. E.g. in case of one buyer and two sellers, two forms have to be filled in and for two buyers and two seller, four forms have to be filled in for respective property shares.

What is Fee in Form 26QB and when is it applicable?As per section 234E of the IT Act, 1961 read with Rule 31A (4A) of IT rules, 1962, failure on the part of taxpayer to furnish challan-cum-statement in Form No. 26QB electronically within seven days from the end of the month in which the tax deduction is made will attract levy of fee to be paid by the buyer/transferee/payer.

I have filled Form 26QB and made the payment online, but I forgot to save the Acknowledgment Number generated at TIN website. From where can I get the Acknowledgment Number.?a) Acknowledgment number for the Form 26QB furnished is available in the Form 26AS (Annual Tax Statement) of the Deductor (i.e. Purchaser/ Buyer of property). The same can be viewed from the TRACES website (www.tdscpc.gov.in) orb) Taxpayer can also click the option ‘View Acknowledgment’ hosted on the TIN website. Taxpayer needs to enter PAN of the Buyer and Seller, Total Payment and Assessment Year (as mentioned at the time of filing the Form 26QB) to retrieve the Acknowledgment Number.

What is Form 16B?Form 16B is the TDS certificate to be issued by the deductor (Buyer of property) to the deductee (Seller of property) in respect of the taxes deducted and deposited into the Government Account.

What is Form 26QC?Form 26QC is the challan-cum-statement for reporting the transactions liable to TDS on rent under section 194-IB of the Income-tax Act, 1961. It is an online form available on the TIN website.

The Finance Act, 2017 has introduced section 194-IB providing that Tenant of a property making monthly rent payment exceeding ₹ 50, 000 is required to deduct tax at the rate of 5% from the rent payable to a resident landlord (depending upon the Date of Payment/Credit to the Landlord).

The tenant of the property being an individual or a HUF (not liable to audit u/s 44AB) would have to deduct the TDS and deposit the same in Government treasury.

What is Form 16C?Form 16C is the TDS certificate to be issued by the deductor (Tenant of property) to the deductee (Landlord of property) in respect of the tax deducted and deposited as TDS on rent under section 194-IB of the Income-tax Act, 1961.

What is the periodicity of filling Form 26QC?According to rule, Taxpayer/Tenant should furnish challan-cum-statement in Form 26QC in following scenarios:-At the end of the FY or in the month when the premise is vacated / termination of agreement. However, taxpayer has to mandatorily file the Form at the end of each Financial Year (in case the agreement period contains more than one FY and rent has been paid/credited during the year)

In the month when the premise is vacated/ termination of agreement ( in case the agreement period falls in the same FY)

Example 1 (Rent Agreement falling across two FY):- Tenant Mr. A has entered into a tenancy agreement with Landlord Mr. X for the period of 11 months from October 1, 2017 to August 31, 2018 @ rent of Rs. 60,000.

Explanation: - In this case, Mr. A should file Form 26QC twice i.e. firstly at the end of the FY 2017-18 (on March 31, 2018) and secondly at the end of the tenancy period (on August 31, 2018). Following values will be captured in the below fields:

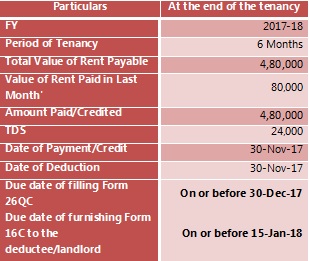

Example 2 (Rent Agreement falling in same FY):- Tenant Mr. B has entered into a tenancy agreement with Landlord Mr. Y for the period of 6 months from June 1, 2017 to November 30, 2017 @ rent of Rs. 80,000 for 6 months.Explanation: - In this case, Mr. B will have to file Form 26QC only once i.e. at the end of tenancy period (on November 30, 2017). Following values will be captured in the below fields:

What is Form 26QD?Form 26QD is the challan-cum-statement for reporting the transactions liable to TDS on PAYMENTS TO RESIDENT CONTRACTORS AND PROFESSIONALS under section 194M of the Income-tax Act, 1961. It is an online form available on the TIN website.

What is the due date of payment of TDS deducted on payment ‘TO RESIDENT CONTRACTORS AND PROFESSIONALS’ u/s 194M?The due date of payment of TDS on ‘PAYMENTS TO RESIDENT CONTRACTORS AND PROFESSIONALS’ is within a period of thirty days from the end of the month in which the payment has been made.

Example: If Date of Payment is September 1st, 2019, then due date for filing Form 26QD will be October 30, 2019’.

What is the periodicity of filling Form 26QD?According to rule, Payer / Deductor should furnish challan-cum-statement in Form 26QD in following scenarios:- At the end of ‘Financial Year’ At the end of ‘Termination of Contract/Services’

Both cases or at the time of Payment/Credit deductor/payer can file 26QD

Explanation: If Date of Payment is September 1st, 2019, then due date for filing Form 26QD will be October 30, 2019’

What is Form 16D?Form 16D is the TDS certificate to be issued by the deductor to the deductee in respect of the tax deducted and deposited as TDS under section 194M of the Income-tax Act, 1961.

The furnishing of information for payment to Non-Residents not being a Company, or to a Foreign Company in Form 15CA has been classified into 4 parts. Depending upon the case, you will need to fill the relevant part.

I just wanted to say this is an elegantly composed article as we have seen here. I got some knowledge from your article and also it is a significant article for us. Thanks for sharing an article like this.Tds Filing in Chennai

ReplyDelete